By Tim Farrelly – CEO of Farrelly’s, and asset allocation consultant to Australian Unity Personal Financial Services

Many investors fear the impact of a return to interest rates of 5%, 6% or even 7%pa that were considered normal just a few years ago. They worry about the impact on share and property markets, they worry about locking fixed rate term deposits and annuities and missing out on the big rate rises to come.

Others are worried about their ability to service borrowings if interest rates move sharply higher.

Yes, interest rates will not be this low for ever, but rate rises are likely to be modest and temporary. As for 7% cash rates, we are unlikely to see them again for decades.

Why?

It is because cash rates are set by the Reserve Bank of Australia (RBA) in order to moderate the growth of the Australian economy and keep inflation in check.

When the Reserve Bank increases interest rates, they hope to slow the economy and thus ease inflationary pressures. The former Governor of the RBA, Glenn Stevens, observed a year ago, that the impact on the Australian economy of interest rate rises is predominantly felt at the household level rather than at the business level.

This is because households with mortgage debt have their spending ability rapidly affected when mortgage interest rates rise while businesses do not normally change their spending plans with every 0.25% change in interest rates.

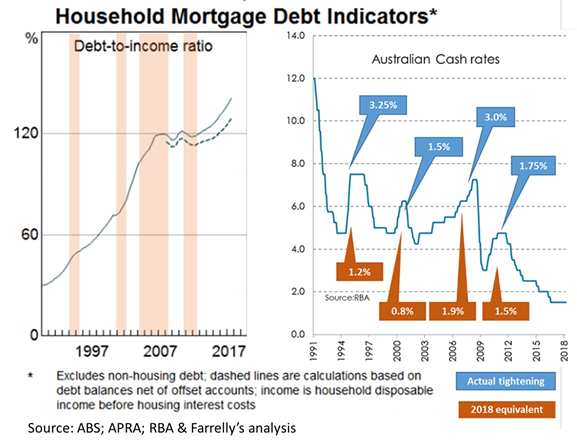

Now, the level of mortgage debt in Australia has risen dramatically over the past 30 years. The left-hand side of the chart below shows the level of household mortgage debt as a percentage of household income since 1992 with the bars in the chart showing the four periods where the RBA increased cash rates.

What we see is that household debt rose from 45% at the time of the first rate hike in 1994, to 120% at the time of the most recent increase, to 139% today. What this means is that a 1% interest rate increase today has around three times the impact on household finances that it would have had in 1994.

The right-hand side of the chart below shows the actual size of the past four rate rises and, given the increase in the level of household debt since that rise, what increase in interest rates would be required today, to have the same effect on the economy.

What we see is that, historically, an equivalent of a 0.8% to 2.1% increase in interest rates has been enough to cool the economy sufficiently to bring inflation under control.