The Federal Treasurer Scott Morrison (or ‘ScoMo’ as he’s more affectionately known) delivered the 2018-19 Federal Budget on Tuesday night. The budget indicates an expected return to surplus in 2019-20. Amongst the pages of detail and myriad of changes handed down, we’ve summarised the key changes that we believe will impact most on individuals and small business.

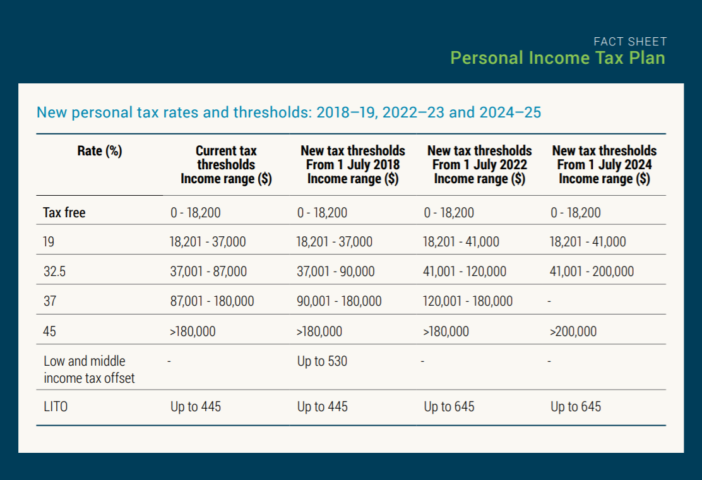

Tax Cuts: While there was little in the way of confirmed tax cuts for companies, individual taxpayers will benefit from a proposed raft of changes to tax thresholds and low income tax offsets, to take effect progressively over the next 7 years. These changes are summarised in the table below:

The proposed tax cuts are likely to benefit 10 million Australian taxpayers, possibly pointing to the announcement of an early election. The tax cuts will create a single tax rate of 32.5% for workers earning between $41,000p.a. and $200,000p.a. The flow on effect means that 94% of taxpayers will pay no more than 32.5c in the dollar (as opposed to 63% currently). All this at a cost of $140 billion over 10 years.

Medicare Levy:

A proposed increase in the Medicare Levy from 2.0% to 2.5%, that was announced in the 2017-18 budget and intended to take effect from 1 July 2019, has now been removed.

Small Business Asset Write-Off:

The provision allowing businesses with turnover of up to $10 million to immediately write-off assets costing less than $20,000 was extended for a further year.

Cash Economy:

Cash payments to business will be restricted to $10,000 or less. Any payments over $10,000 will need to be made via the banking system (electronically or via cheque). This is a clear crackdown on the cash economy, allowing the government to better track and cross-match payments to businesses with amounts declared in returns.

Work-Related Expenses:

The ATO crackdown on work-related expense claims is expected to continue, with the ATO handed significant extra funding to focus on these claims. Taxpayers be warned!

Deductions for Vacant Land:

Expenses associated with holding vacant land will cease to be deductible from 1 July 2019 and will not be able to be carried forward.